If you question whether you are wasting money renting, this blog post is for you. Afterall, no discussion on housing is complete without the rent vs buy debate.

In reality, it hardly ever is an actual debate thanks to the popular cliche that renting is a big waste of money. Such platitudes are so prevalent that they’ve convinced us that renting is always throwing away money or that buying is unequivocally better than renting.

But are these cliches actually true?

This article will solve the rent versus buy discussion by providing an analysis grounded in facts and cold hard data.

From here, we will be able to dismiss the notion that renting is the inferior choice and a waste of money compared to buying. We can also embrace renting as a solid choice along our financial journeys.

Contents

Is Renting Really A Waste Of Money?

As I’ve mentioned previously, renting is worthwhile option because of the value it provides us in terms of utility and satisfaction from having a place to live in and enjoy.

Utility and satisfaction are intangible benefits of renting which may be difficult to quantify or value. Be that as it may, nearly everyone can appreciate data proving that renting is not a waste of money.

So with that, let us get on with our analysis.

Mortgages Are Investments That Build Equity

Most arguments for why renting is a waste of money hinge on the fact that homeowners with mortgages build equity, and thus possess a valuable investment.

While it is true that homeownership builds equity, it is equally true that a significant portion of equity growth is offset by costs associated with owning that renters avoid.

A more detailed cost benefit analysis reveals that the investment potential associated with homeownership is likely blown out of proportion.

Let’s use a real life scenario to see how this plays out.

In this example, we will compare the full scope of costs associated with owning a home versus renting over the typical 30 year period that most mortgages last.

Owning Vs Renting: Assumptions

- Single family primary residence. No rentals, house hacks, Airbnb etc.

- Home purchase price of $300,000 to reflect the median purchase price in January 2017.

- 30-year fixed rate mortgage. Average of 3.71% in the United States for years 2017 – 2021.

- Starting median gross rent of $1,163 with an annual increase of 2% to reflect the Federal Reserve’s annual inflation target.

- Starting average homeowners insurance of $1,211 to reflect the 2017 average with 2% annual inflation increase.

- Starting property tax rate of 1.17% to reflect 2017 effective property tax rate. No increases over this period.

- Maintenance costs fixed at $3,000 annually using the 1% rule.

- Renters insurance of $180 to reflect the 2017 average.

- Buyer’s closing costs of 4%.

- Utility costs ignored as they are assumed by owners and renters.

| Financial Breakdown: Is Renting A Waste Of Money? | |

|---|---|

|

Owning |

Renting |

|

Purchase Price: $300,000 |

Rent Deposit (2x rent): $2,326 |

|

Down Payment: $60,000 |

First Year Rent Monthly: $1,163 |

|

Mortgage Balance: $240,000 |

First Year Rent Total: $13,956 |

|

Interest Rate: 3.71% |

Annual Renters Insurance: $180 |

|

Monthly Mortgage Payment: $1,383 |

Total Cost In First Year: $14,136 |

|

— |

— |

|

Total Out Of Pocket Costs Over 30 Years: $688,164 |

Year 30 Rent Monthly: $2,065 |

|

Year 30 Rent Total: $24,784 |

|

Annual Renters Insurance: $180 |

|

Total Cost In Year 30: $24,964 |

|

— |

|

Total 30 Year Cost Assuming 2% Annual Rent Increase: $573,894 |

|

|

As we can see, the person renting at the median price in 2017 spends $114,270 less than the median homeowner over the course of 30 years.

There are several reasons for this.

For starters, the renter had lower upfront costs since they didn’t expend the hefty down payment that homeownership requires. Additionally, the homeowner incurred other costs associated with owning such interest fees, homeowners insurance, property taxes, closing costs, and maintenance.

No one ever seems to mention these fees when talking about the merits of homeownership. They simply mention how much equity they’ve built without ever mentioning the offsetting out of pocket costs.

Price Appreciation Makes Homeownership The Better Choice

True, homeowners do typically enjoy value growth from property ownership. At the same time, homeowners incur steep costs that offset much of these gains. Let’s use the homeownership numbers above to illustrate how this works.

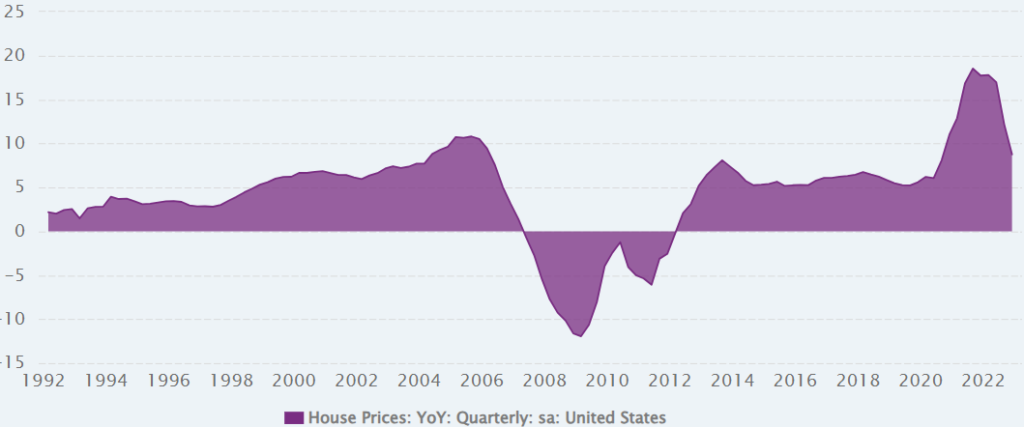

For this example, we will assume that the owner’s house appreciates at a rate of 5.4% annually. This rate of growth reflects average home price growth in the United States from 1992 – 2022.

You’ll see in the breakdown that the home’s value grows 5x over the 30 year period. Not bad! In spite of this impressive growth, you will see that the majority of gains are offset by steep costs that accumulate over the years.

Most homeowners don’t keep annual cash flow statements and balance sheets, which explains why it is so easy for them to assume that their homes are money making machines. While homes do gain in value, they don’t produce net profits that many think.

| Equity Growth From Homeownership vs Costs |

|---|

|

Starting Home Value: $300,000 |

|

Home Value In Year 30: $1,453,247 |

|

— |

|

Total Out Of Pocket Costs Over 30 Years: $$688,164 |

|

|

|

|

|

|

|

Net Profit From Owning: $785,083 |

This Already Proves That Renting Is Better Than Owning, Right?

Well, not exactly. There is more to the story.

For starters, profiting nearly $800,000 on a home is no small feat. And this is precisely why many people argue the merits of homeownership. It is indeed a great long term investment to have.

Be that as it may, the goal of this article is to prove that renting is not a waste of money relative to owning. Therefore, we must round out our analysis with consideration for the investment opportunities gained from being a renter.

Opportunity Costs Of Owning

That is, we will consider the opportunity costs of owning by exploring how else the money involved with owning could be used.

We’ll do that by looking at a scenario where the renter in our initial scenario invests the savings gained from renting into the stock market over the same 30 year period.

We will assume that the renter invests the down payment amount of $60,000 toward a common index fund instead of investing in a home purchase. The renter also spreads the $114,270 savings from renting equally into the index fund over the 30 year period. This amounts to $3,890 per year contributed at the beginning of each year.

From here, we can fully assess whether renting is truly a waste of money or if it presents a wonderful opportunity to invest and build wealth.

| Potential Investment Returns While Renting |

|---|

|

Index Fund: VANGUARD TOTAL STOCK MARKET INDEX FUND ADMIRAL SHARES(VTSAX) |

|

— |

|

Initial Investment: $60,000 |

|

Annual Contribution: $3,890 |

|

— |

|

Account Value After 30 Years: $1,787,607 |

Potential Net Worth Of The Renter Renter Vs The Homeowner

The above scenarios prove that a renter could potentially the renter could very well come out ahead over the homeowner after 30 years. More specifically, the renter has a net worth of $1,787,607 which is $334,360 higher than the median homeowner who has a respectable net worth of $1,453,247.

But Moses, this sounds all wrong. There must be an error in your analysis. How can this be?

I’ll start by saying you should run the numbers yourself to determine the accuracy of my analysis. Further, you should always run such scenarios using your actual numbers to determine what is best.

That said, let me pose a few reasons why renting could be a better choice than buying

Stocks Outperform Real Estate

Predictably, a majority of Americans believe that real estate is the best long term investment vehicle. This is likely due to the fact that real estate provides a stable and reliable investment relative to other options such as stocks.

Even so, we must recognize the fact that the stock market has historically outperformed real estate.Let’s turn to Investopedia for more:

Consider the 47 years between 1975 and 2022. A $100 investment in the average home in the fourth quarter of 1975 would have grown to about $928 by the first quarter of 2022.6. A similar $100 investment in the S&P 500 at the beginning of 1975 would yield approximately $19,351 in 2022, provided all dividends were reinvested.

Renting Is Cheaper Than Owning

As it currently stands in August 2023, renting is cheaper than buying in 99.97% of cities in the United States. In simpler terms, there are only 4 cities where it is cheaper to buy than rent on a monthly basis.

We may be tempted to dismiss this as a function of currently high interest rates, but rent has generally always been cheaper than buying with the exception of a few years.

But A Mortgage Is Temporary Rent Lasts Forever

One of the main reasons for people saying that renting is a waste of money is that mortgages typically last between 15 – 30 years while renting goes on indefinitely. The idea of having free housing at some point in our lives is an attractive lure for owning.

It is indeed true that mortgages are temporary. Conversely, it is also true that there is no such thing as free housing under most circumstances. In other words, a mortgage is only a part of the costs involved with homeownership with additional costs that last forever.

These costs, notably maintenance, taxes, and insurance can be substantial. They can also add up to rival the cost of rent – even when the mortgage is paid off.

The following table shows how the ongoing costs of ownership can stack up.

| Ongoing Monthly Cost Without A Mortgage |

|---|

|

Initial Home Value: $300,000 |

|

Home Value In Year 30: $1,453,247 |

|

Mortgage Payment: $0 |

|

Property Taxes: $292 |

|

Maintenance: $250 |

|

Repairs: $600 |

|

Homeowners Insurance: $179 |

|

HOA Fees: $350 |

|

Utilities: $400 |

|

Total Monthly Costs: $2,071 |

As we can see from above, the ongoing costs of homeownership can be steep – even with a paid off house. At $2,071, these costs add up to be slightly more expensive than what the renter in our above scenario is paying after 30 years of rent increases ($2,065).

The True Costs Of Homeownership Are Really High

If you don’t believe these numbers are possible, I’ll use the words of legendary personal finance blogger, Financial Samurai, and say that it pays to think in extremes. The last thing I’d want you to do is underestimate your ongoing housing costs, and then find yourself stretching a fixed retirement budget just to make ends meet.

Notwithstanding, these figures may seem high – but reality shows they are quite reasonable.

For example, my home state of Florida has an average HOA fee between $300 – $400 per month as reflected above. Plus, the wise among us will heed the fact that these fees typically rise each year.

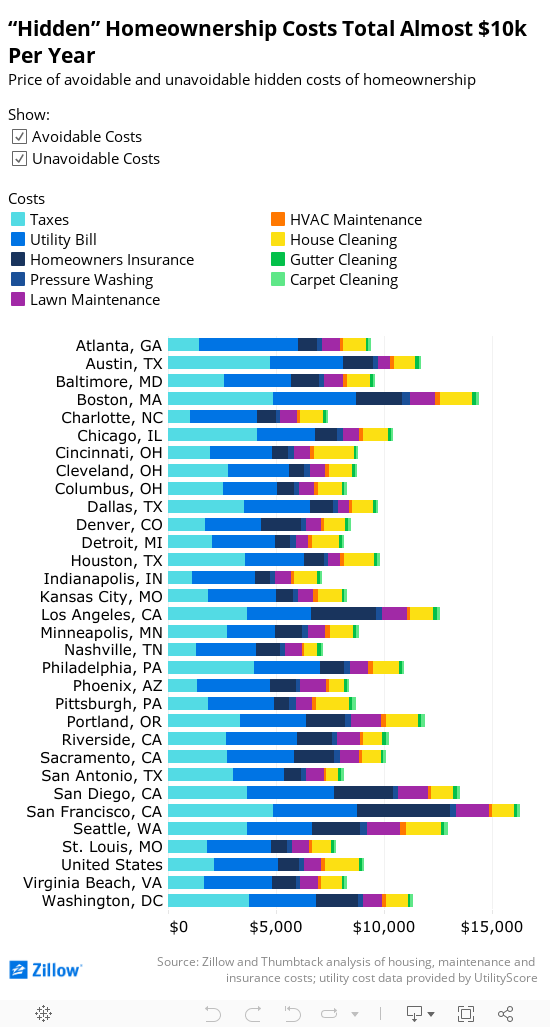

Zillow and home renovation platform Thumbtack found that essential home maintenance projects average $6,413 annually. Of course, that can vary greatly depending on where you reside. But throw in other ongoing expenses, like property taxes, utilities and homeowners insurance, and you could be facing five figures’ worth in annual outlay.

In terms of repairs, $600 per month may seem like a lot of money until we consider the substantial cost to fix practically any large feature of a home. A study by Zillow and Thumbtack confirms as much as they show that repair costs can range from $6,000 – $9,000 per year. This is reflected in the repair amount above and the graph below.

You Pay Someone Else's Mortgage So Renting Is A Waste Of Money

To this, I say, it could be true.

I also say, who cares and what’s your point?

Seriously, why be concerned with who has the privilege of owning the debt and a liability against a property? Even with the benefit of equity growth and value appreciation, why would we care that someone else is making an investment they deem worthwhile.

Plus, it may not even be true that you are paying someone else’s mortgage in a case where you rent from one of the 40% of owners without a mortgage.

Simply put, both renting and owning serve the same basic function which is to provide shelter. We can start to pick apart the fringe benefits as demonstrated above, but these extend beyond the basic function of providing housing.

When you rent, you pay an owner for the privilege of staying at their property. When you own, the holder of the note is the owner, thus you pay them for the same privilege. Once owned outright, you become the owner and still have to deal with ongoing costs as mentioned above.

In sum, renting and owning both result in housing. Beyond that, it becomes a matter of tradeoffs for the best use of your hard earned cash.

The Problem With Renting Are The High Prices

Therefore owning is better, right? Whoah, let’s pump the brakes before we jump to illogical conclusions about rent prices and owning.

Rent prices rose at a sharp 16% from 2020 – 2022 as a result of inflation, increased demand, and low inventory. Seeing your rent rise so dramatically over a 1-2 year period can be jarring for many. I personally know people who are impacted in this manner. My sister, for example, faced a 1 year rent increase of about $600 to stay in her 2 bedroom apartment in Tampa.

As a result of these increases, it is easy for us to point to this trend as justification for why owning is a better choice than renting.

But is it actually true? I’ll let you be the judge.

Rent Price Increases Were Offset By Home Price Increases

What is often left out of the rent versus buy discussion is that owning and renting both exists under a general housing umbrella. As a result, the prices across both typically flow in the same direction.

In economics, renting and owning would be considered substitute goods which essentially means they can be used interchangeably to fill the same need. Both satisfy the need for housing and are therefore subject to the basic forces of supply and demand.

As home prices rise, rent prices also tend to rise and vice versa.

Rents Rose 16% & Home Prices Rose 30%

As previously mentioned, rent prices sharply rose by an average of 16% across the nation. Alongside rent price surges, home prices rose by even greater magnitudes over the same period.

Just how big was the home price increase? Data from the Federal Reserve shows that home values rose by 30% from 2020 – 2022.

Sure, facing a 16% rent increase is jarring. But this is no justification for opting for a home that costs 30% more than it did in the previous year solely because of increased demand.

In simple numerical terms, a person who rents for $1,000 per month facing a 16% rent increase would now have to pay $1,160 per month. If this person looked to buy a house that cost $300,000 a year ago, they would now have to pay $390,000 for the exact same property.

Rent Price Increases Vs Upfront Costs Of Owning

As rent prices rise, the renter’s out of pocket monthly costs also rise. Using the example above, the person paying $1,000 in 2020 would have been paying $1,160 by 2021.

Let’s assume they found these rent increases unacceptable and opted to purchase instead. We already know they would have been buying a home that was 30% more expensive – but is that the full picture?

To fully assess, we must consider the upfront costs associated with owning relative to renting. The person in our example could very well stay put and incur the additional $160 out of pocket each month. Or, they could buy and fork over the down payment, realtors fees, closing costs, and ancillary costs such as inspections and moving.

Using current averages, the total out of pocket costs for a $390,000 home purchase can amount to a steep $118,591 up front broken down as follows:

- Purchase Price $390,000

- Down Payment: $78,000

- Realtor Fees: $23,400

- Closing Costs: $15,600

- Inspections: $341

- Moving Costs: $1250

Emotionally Charged Homebuying

No one likes rent increases. But responding to a 16% rent increase by opting for a home purchase at such steep upfront costs and long term implications is likely an emotionally driven decision.

Well, when it comes to all of our financial decisions, my best advice is for you not to trust your instincts, to just accept the idea that we're all kind of crazy when it comes to money. And so having some curiosity about whatever it is, if you have a sudden desire or you feel this urgent need to buy a home, you want to engage your prefrontal cortex, because what's happening is, it's emotional.

The Psychology of Homebuying - Wall Street Journal

Rent Prices Don’t Increase Forever

Some people may interpret several years of rent increases as a sign that rental prices rise in perpetuity or that they will increase by the same magnitude each year. In reality, this doesn’t happen as rents usually move according to supply and demand.

We’ve already seen some months this year with rent decreases relative to the same month last year . For example, May saw a 0.5% decrease in median rents across the nation compared to last year. Sure half a percent isn’t much, but it shows that rents do in fact decrease at times.

Further, rents are projected to fall further thanks to increased supply via significant multifamily construction we are starting to see. As more units hit the market, prices of existing properties will come down to remain competitive given the increased supply.

But I have A Low Interest Rate, So I’m Lucky

Kudos to you for having a low interest rate. You should rejoice and be thankful for your fortunate situation. You should also take advantage of it by ensuring you are on track with your finances.

Notwithstanding, one of the downsides of having an extremely low interest is the lock in effect it can produce. A survey by Realtor.com shows that 82% of respondents feel stuck in their homes thanks to the fact that interest rates have now risen.

Going from a 3% mortgage, to a 6% mortgage can be costly and prohibitive. As a result, many homeowners are trapped in their homes thanks to what has been referred to as “the golden handcuff” effect.

Not being able to move because of a low interest is no way to live in my humble opinion. Meanwhile, renters enjoy maximum freedom of mobility which is a major tenet to my definition of a free life.

Is Renting A Waste Of Money?

As shown in this post, renting is unequivocally better than owning across several dimensions. Renting has lower upfront costs and is less costly on an ongoing basis. Renting also provides greater freedom and flexibility.

If taken advantage of properly, renters can come out substantially better from a financial perspective than homeowners. The operative words being if taken advantage of properly.

Unfortunately, most renters don’t capitalize on the advantageous position. By the numbers, we see that most homeowners build significantly more wealth than renters over the long haul.

Rather than embodying ideals such as my success stacking principle, most renters squander their positions by spending the cost savings elsewhere. Meanwhile, homeowners consistently build equity and enjoy price appreciation as shown above.

Where Homeownership Shines Over Renting

In the words of Paula Pant at Afford Anything, your home is a lousy investment. This is because real estate typically underperforms relative to other investment options such as stocks.

That said, homeownership shines and works for many because of the forced savings vehicle it creates. Most people simply lack the discipline to save and invest over the long haul. Thus, having a mortgage forces us to do it without thought.

Additionally, the act of purchasing a home is much more accessible than learning to invest. Most people are turned off from effort and risk involved in other forms of investing. In essence, owning a home is just the easier choice overall.

Finally, real estate is a much safe investment due to the lower volatility and risk that one experience in the stock market. This is why it is so important for us to actually learn to be wise investors.

Rent Or Buy Cliches Vs Reality

Cliches are useful because they are quick and easy for breaking down complex subjects into simple heuristics. The claim that renting is a waste of money is one such declaration.

Homeownership may be the American dream but blindly claiming it is the unequivocal best route is significantly flawed and plainly untrue.

Renting truly is a viable option that could result in much greater financial success. This post has proven that with a more detailed analysis of whether homeownership or renting is the optimal financial decision.

Armed with this information, you are now better able to make an informed decision on what financial path is best for you. Afterall, we can have a lot of things in life, but we can’t have them all.

One Response

Thanks for the comment, Bob! You’ve done quite well it seems and are probably more of an exception to what is commonly seen. If I were to buy a house, I’d do it just like you and get it paid off as early as possible. But I personally don’t like being in debt, so my approach would be to save money and make a cash offer which should actually be rewarded in a better deal and without having to pay years of mortgage interest. Also, as a renter you could be “living” in the same house and sitting on $350,000 worth of investments without the albatross of the house. But like I said, if I were to own, I’d go cash or go your route and pay if off quickly.